The Australian SMSF mortgage market has reached a critical juncture. What began as a cautious experiment in 2007 has matured into a sophisticated financing ecosystem, with over 11% of self-managed super funds now utilizing Limited Recourse Borrowing Arrangements (LRBAs) to acquire property assets. For SMSF trustees contemplating their next property investment, understanding the current mortgage market shifts isn’t just helpful—it’s essential.

The landscape has transformed dramatically since 2024. Rising interest rates have pushed SMSF loan rates into the 6.5-7% range, with some lenders charging even more. At the same time, lender expectations have tightened considerably. The handful of banks and non-bank lenders still actively offering SMSF loans are scrutinizing applications with unprecedented rigor, focusing intensely on serviceability, cash flow projections, and compliance with ATO regulations.

This isn’t your father’s property investment market. The combination of higher borrowing costs, stricter lending criteria, and evolving regulatory guidance means trustees must approach SMSF property investment with clear eyes and comprehensive strategies. The opportunities remain substantial—but so do the risks for those who proceed without adequate preparation.

Understanding the Fundamentals: SMSF, LRBAs, and Safe Harbour Rates

Before diving into market conditions, let’s establish the foundational concepts that govern SMSF property lending.

A Self-Managed Super Fund is exactly what it sounds like—a superannuation fund that you manage yourself, rather than leaving to a traditional fund manager. With average assets per SMSF member sitting at $881,000 and average total fund assets reaching $1.6 million, these vehicles represent significant investment firepower for property acquisition.

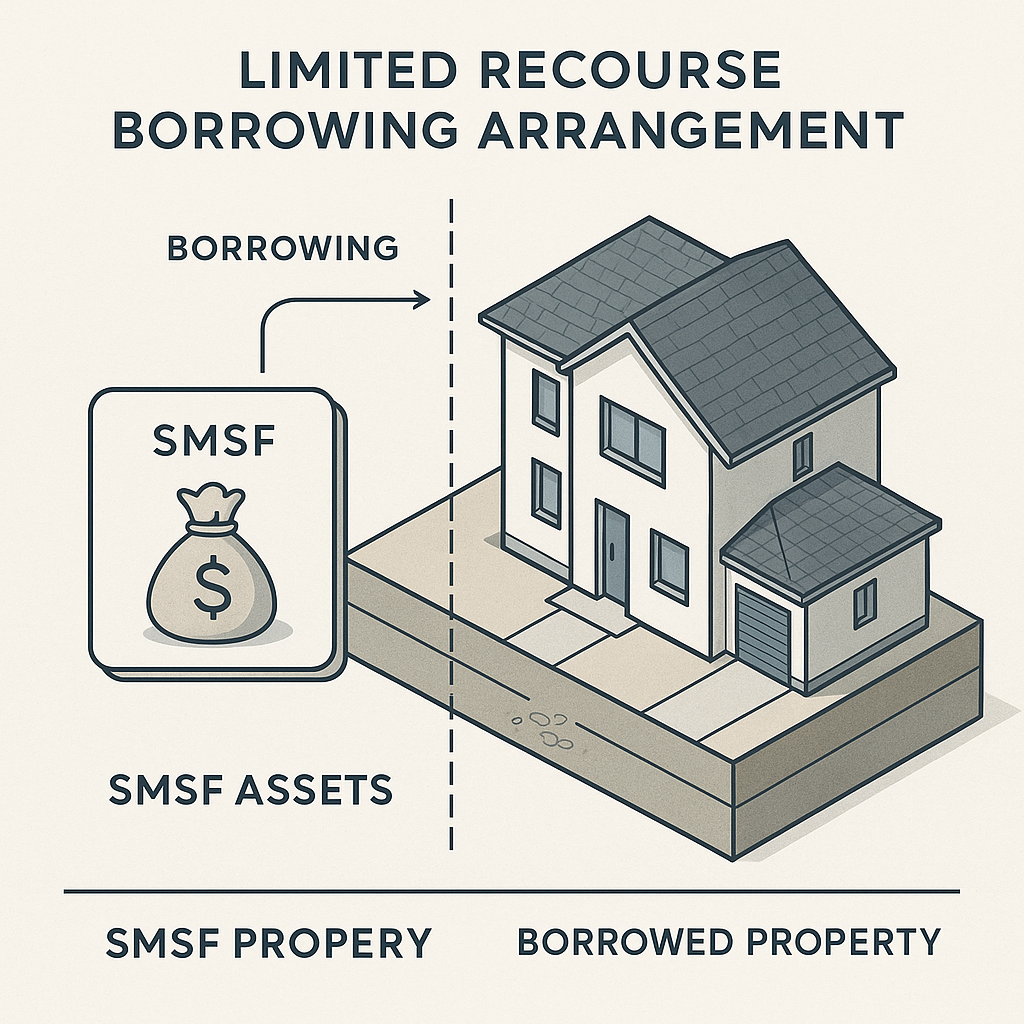

Limited Recourse Borrowing Arrangements are the mechanism that makes SMSF property investment possible. Under an LRBA, your SMSF can borrow money to purchase an asset, but the lender’s recourse is limited to that specific asset if things go wrong. This protects your other superannuation assets from being seized to cover the debt—a crucial safeguard built into the SMSF lending structure.

Safe harbour interest rates, published quarterly by the Australian Tax Office, represent benchmark rates for related-party loans within SMSFs. These rates matter because they establish what the ATO considers commercially reasonable borrowing costs. Even if you’re borrowing from an unrelated commercial lender, these rates influence the broader market and provide a compliance benchmark.

The LRBA market size has grown substantially. SMSF investment in residential properties reached $57.5 million in September 2024, while commercial property investments hit $107.6 million. These figures might seem modest compared to Australia’s $10.8 trillion residential property market—representing just 0.7% market share—but they reflect billions of dollars in leveraged superannuation assets.

One significant recent change is the Transfer Balance Cap increase, which raised the maximum amount Australians can transfer into retirement phase from $1.6 million to $1.9 million. This expanded capacity means more SMSF trustees can potentially consider property investments without breaching their caps, creating additional market demand.

The Current Market Snapshot: 2024-2025 Realities

The SMSF mortgage market today operates under conditions that would have seemed extraordinary just three years ago. The rising uptake of LRBAs has been notable, with SMSF loans becoming increasingly popular as people max out their borrowing capacity under their personal names. This trend reflects a broader shift: savvy investors recognizing that superannuation can offer a tax-advantaged pathway to property ownership when traditional lending channels reach their limits.

However, this increased demand has collided with constrained supply. The number of lenders actively offering SMSF loans has contracted significantly. Those remaining charge a substantial premium, with headline SMSF rates currently sitting between 6.5% and 7%, compared to rates starting from 6.24% at specialized lenders like Aries Financial. This premium reflects both the complexity of SMSF lending and the heightened risk perception among traditional financial institutions. For trustees seeking competitive alternatives, exploring non-bank lenders can reveal more flexible financing solutions.

Rate increases have created ripple effects throughout the market. Property valuations have come under pressure as higher interest rates compress capitalization rates and reduce buyer purchasing power. Rental markets, while remaining strong in many locations, haven’t universally kept pace with the increased debt servicing costs that SMSF trustees face. Queensland, for instance, saw average SMSF loan sizes peak at $811,000 in December 2024 before declining to $795,000 by March 2025—a small but telling indicator of market adjustment.

The underwriting criteria tightening represents perhaps the most significant shift. Lenders now demand more comprehensive documentation, more conservative rental income projections, and larger cash reserves within the SMSF structure. Where a 90% loan-to-value ratio was once achievable for well-positioned funds, many lenders have pulled back to 80% or even 70% LVRs for certain property types or locations. This conservatism reflects lessons learned during previous rate cycles and a more cautious approach to SMSF risk profiles.

The Lending Environment: Rates, Returns, and Serviceability

Understanding the current lending environment requires looking beyond headline rates to the underlying economics of SMSF property investment.

The safe harbour LRBA rates published by the ATO provide an important baseline. These rates, while not mandatory for arm’s-length commercial loans, influence what the market considers reasonable. When safe harbour rates rise alongside general interest rate movements, they validate higher commercial lending rates while simultaneously affecting the compliance calculations for related-party loans.

Market yields have compressed significantly. A property that might have offered a 5.5% gross rental yield three years ago may now achieve only 4.5-5%, while borrowing costs have moved in the opposite direction. This yield-to-rate squeeze puts enormous pressure on cash flow and serviceability.

Serviceability calculations have become make-or-break factors. Lenders typically assess whether the SMSF can service the loan from rental income plus available cash reserves, applying stress test rates 2-3% above the actual loan rate. With assessment rates potentially reaching 9-10%, properties must generate substantial income or the SMSF must hold significant cash buffers to satisfy lender requirements.

At Aries Financial, we’ve seen firsthand how these dynamics affect trustees. Our fast approval process—typically 1-3 business days—reflects our specialized understanding of SMSF lending compliance and our ability to quickly assess whether a proposed investment structure will meet both lender serviceability requirements and ATO compliance standards. This expertise becomes invaluable when every percentage point matters and timing can determine whether an opportunity is captured or lost.

Regulatory and Compliance Considerations

The regulatory backdrop for SMSF property investment continues to evolve, with the ATO maintaining explicit expectations around LRBA usage and compliance.

The fundamental question facing many trustees is whether LRBAs remain viable amid tighter regulatory controls. The answer isn’t simple. While the ATO hasn’t moved to eliminate LRBAs—they remain a legitimate investment strategy—the regulator has made clear that arrangements must serve genuine retirement purposes rather than early access schemes or impermissible present-day benefits. Understanding LRBA compliance rules is essential for protecting your fund.

Specific updates for 2025 have reinforced this stance. The ATO has provided clearer guidance around short-term borrowing arrangements, emphasizing that even temporary loans must comply with LRBA requirements if used to acquire assets. This guidance closes potential loopholes while clarifying what constitutes compliant behavior.

Trustees should understand several key compliance points:

First, all LRBA acquisitions must satisfy the sole purpose test—they must be maintained for the sole purpose of providing retirement benefits to members. Second, the property cannot be acquired from a related party (with limited exceptions for business real property). Third, the asset must be held in a separate trust structure until the loan is fully repaid.

The implications extend beyond just structuring the initial purchase. Ongoing compliance requires proper documentation of all loan terms, market-rate interest charges for related-party loans, and adherence to the single acquirable asset rule—you cannot use borrowed funds to purchase multiple properties simultaneously.

Opportunities and Risks in Today’s Market

Despite the challenges, significant opportunities remain for SMSF trustees willing to navigate the current environment strategically.

Access to property within super provides unique advantages. Tax benefits alone can be compelling—rental income is taxed at 15% during accumulation phase and potentially 0% in pension phase, compared to marginal tax rates up to 47% for property held personally. For high-income earners, this differential creates substantial long-term wealth accumulation advantages.

Diversification potential represents another key opportunity. An SMSF holding only shares and cash is exposed to equity market volatility; adding property creates a more balanced asset allocation. Commercial property, in particular, can offer long-term leases with CPI-indexed rent increases, providing inflation protection that other asset classes may lack.

The ability to leverage superannuation contributions creates additional strategic possibilities. By borrowing through an LRBA, trustees can control a larger asset with a smaller initial capital outlay, allowing superannuation contributions to build equity over time while the property potentially appreciates.

However, the risks demand equal attention. Higher debt servicing costs remain the most immediate concern. An SMSF that commits too much capital to loan repayments may lack the liquidity needed for other expenses, including the minimum pension payments required once members enter retirement phase. This illiquidity risk can become acute if property values decline or rental vacancies extend unexpectedly.

Regulatory complexity poses ongoing challenges. SMSF trustees carry personal liability for compliance breaches, including penalties for unauthorized early access, in-house asset violations, or related-party transaction rules. Professional advice isn’t optional—it’s essential insurance against costly mistakes.

Market risks also persist. Property markets can decline, rental yields can compress, and interest rate movements can transform a marginal investment into a loss-making proposition. The limited recourse nature of LRBAs protects other SMSF assets but doesn’t prevent the loss of deposits and equity if a property must be sold at a loss.

Practical Considerations for Trustees and Advisers

Successful SMSF property investment in the current environment requires careful planning across multiple dimensions.

Aligning loan structures with long-term strategies is fundamental. A 30-year LRBA might seem appealing for its lower repayments, but if SMSF members plan to transition to pension phase within 10 years, the strategy must account for reduced contributions and increased pension payment requirements. Many sophisticated trustees now prefer split arrangements, fixing part of their borrowing for interest rate stability while keeping portions variable for flexibility.

Maintaining robust serviceability assessments throughout the loan life is crucial. Initial serviceability at loan origination is only the starting point. As members age and contribution patterns change, the SMSF’s capacity to service debt evolves. Regular reviews—ideally annually—help identify potential issues before they become crises.

Staying informed about regulatory changes deserves ongoing attention. The SMSF regulatory environment isn’t static. Legislative changes, ATO guidance updates, and court cases continually shape what is permissible and prudent. Trustees who treat compliance as a one-time exercise rather than an ongoing commitment risk significant problems.

Engaging with qualified advisers provides essential perspective. The right advice team includes a specialized SMSF accountant, a financial adviser with SMSF expertise, and potentially a lawyer for complex trust structures. At Aries Financial, we’ve built our reputation on understanding the complete SMSF lending picture—not just approving loans, but ensuring the entire structure serves our clients’ long-term retirement objectives while maintaining compliance.

Investment Strategies and Decision Criteria

Developing sound investment strategies requires systematic evaluation against clear criteria.

Property type selection matters enormously. Residential property remains the dominant choice, with 82% of SMSF property investors preferring residential investments. These properties offer familiar management requirements and strong liquidity. Commercial property, while representing a smaller share, can deliver superior yields and longer lease terms—commercial investments reached $107.6 million in September 2024, reflecting their appeal to certain SMSF strategies.

Location analysis deserves meticulous attention. Properties in high-growth corridors with strong employment fundamentals, infrastructure investment, and demographic tailwinds offer better prospects for both capital appreciation and rental stability. Conversely, properties in declining regions may appear attractively priced but carry elevated risks that SMSF trustees—who cannot easily diversify across multiple properties due to capital constraints—cannot afford.

Yield expectations must reflect current realities. A 4.5-5% gross yield is now considered acceptable in many markets, whereas anything below 4% creates serious serviceability challenges when borrowing costs exceed 6.5%. Net yields—after accounting for property management, maintenance, insurance, and vacancy—matter more than gross figures for determining actual cash flow.

Balancing leverage with liquidity represents a critical strategic consideration. While maximizing leverage might accelerate wealth accumulation in rising markets, SMSFs need sufficient cash reserves to weather extended vacancies, unexpected repairs, or market downturns without forced asset sales. A prudent approach maintains 12-18 months of loan repayments in liquid reserves, even if this means borrowing less initially.

Looking Ahead: The LRBA Market Outlook

The LRBA market’s maturation continues, shaped by interest rate cycles and regulatory oversight that will define the next several years.

Market observers anticipate continued growth in SMSF property investments, albeit at a more measured pace than the explosive growth seen between 2015 and 2020. The fundamental drivers remain intact: Australians understand property, superannuation balances continue growing, and the tax advantages of holding property within an SMSF structure remain compelling.

However, this growth will occur within a framework of evolving lender scrutiny. Banks and non-bank lenders alike are developing more sophisticated risk assessment models specific to SMSF lending. This sophistication should eventually lead to more competitive pricing for well-structured applications while potentially restricting access for marginal cases.

Interest rate cycles will continue influencing market dynamics. If rates decline from current levels, we may see renewed LRBA activity as serviceability constraints ease and yields become more attractive relative to borrowing costs. Conversely, any further rate increases could push marginal SMSF property investments into negative cash flow territory, forcing consolidation and potentially creating opportunities for well-capitalized trustees to acquire properties from distressed sellers.

Regulatory oversight will likely intensify rather than relax. The ATO has demonstrated clear interest in ensuring LRBAs serve their intended purpose. Trustees should expect more detailed reporting requirements, potential audits focusing specifically on LRBA compliance, and continued refinement of rules governing related-party transactions and prohibited arrangements.

For trustees considering property investment through their SMSF, the message is clear: opportunities exist, but success requires expertise, capital discipline, and careful navigation of an increasingly complex landscape. The era of easy SMSF property returns has passed. What remains is a more mature market that rewards those who approach it with professionalism, realistic expectations, and commitment to long-term strategic thinking.

The mortgage market shifts we’re witnessing aren’t temporary disruptions—they represent the new normal for SMSF property investment. Trustees who recognize this reality and adapt their strategies accordingly will be best positioned to leverage their superannuation for meaningful wealth creation while maintaining the compliance and cash flow stability that successful SMSF management demands.