When Sarah decided to use her SMSF to purchase an investment property, her brother offered to lend the fund $400,000 at what seemed like a generous interest rate. It felt like the perfect family arrangement—until the ATO audit revealed the loan didn’t meet arm’s-length requirements. The result? Her SMSF lost its concessional tax status, and she faced penalties that wiped out years of careful retirement planning.

Limited Recourse Borrowing Arrangements have become increasingly popular among SMSF trustees looking to leverage their superannuation for property investment. According to recent industry data, over 6,000 SMSFs now hold property acquired through borrowing arrangements, representing billions in retirement assets. The appeal is clear: LRBAs allow trustees to purchase high-value assets like commercial or residential property without needing the full purchase price upfront. However, when family members or related parties enter the equation as lenders, what seems like a convenient arrangement can quickly become a compliance nightmare that threatens your entire retirement strategy.

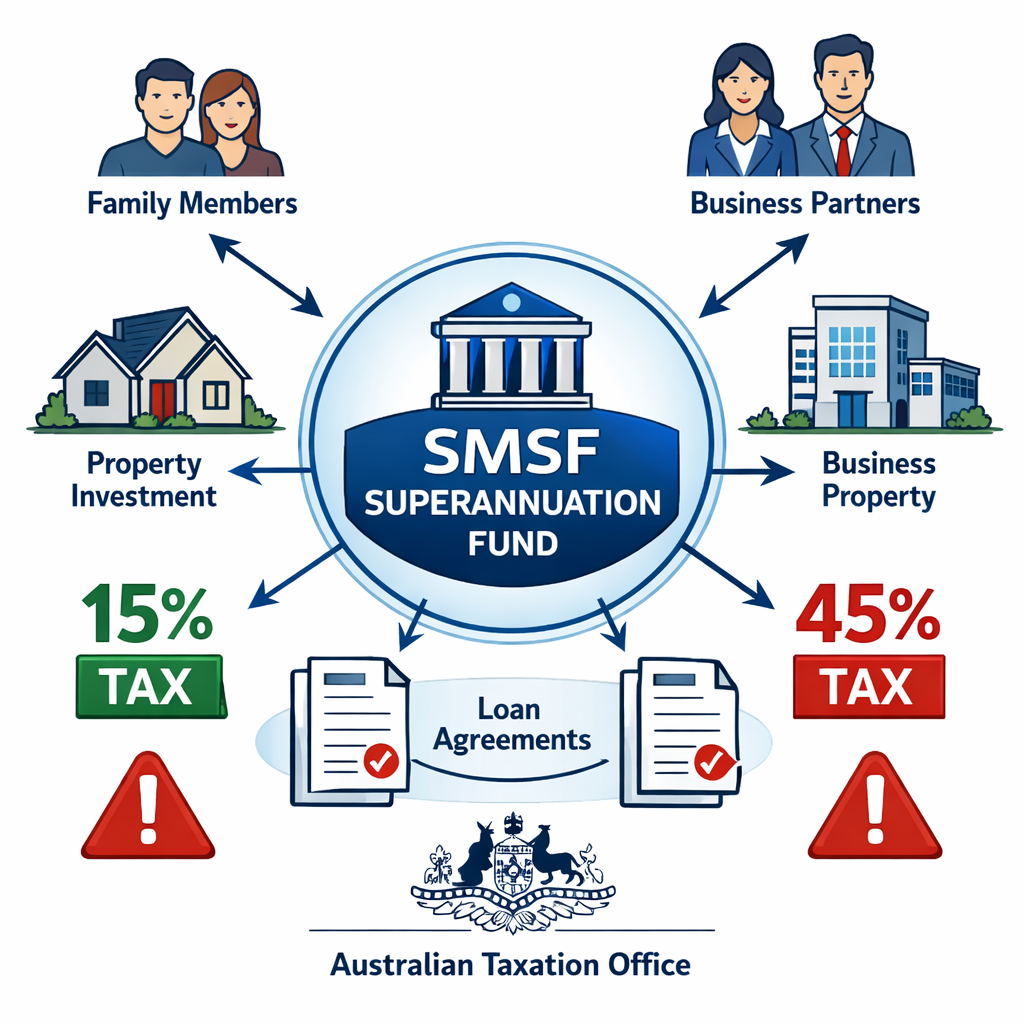

Understanding the compliance and tax implications associated with limited recourse borrowing SMSF related party arrangements isn’t just about following rules—it’s about protecting the wealth you’ve spent decades building. The Australian Taxation Office has been increasingly vigilant in scrutinising these arrangements, particularly when they involve related parties. A single misstep in structuring your LRBA can trigger non-arm’s-length income provisions, potentially taxing your fund’s earnings at 45% instead of the concessional 15% rate. For SMSF trustees considering property investment through borrowing, knowing exactly where the compliance boundaries lie is essential.

Understanding Related Parties in SMSF Borrowing

The term “related party” might sound straightforward, but under the Superannuation Industry Supervision Act, it encompasses a broader network than many trustees realize. A related party includes SMSF members and their relatives, business partners, companies or trusts controlled by members, and any entities where members hold significant influence. When your brother, adult child, family trust, or business associate offers to lend money to your SMSF, they’re stepping into related party territory—and that triggers a specific set of compliance obligations.

The SIS Act permits related parties to provide loans to SMSFs under limited recourse borrowing SMSF related party arrangements, but with one non-negotiable condition: the terms must reflect what independent parties would agree to in the open market. This “arm’s-length” requirement isn’t a suggestion—it’s a legislative mandate designed to prevent SMSFs from becoming vehicles for preferential family deals that undermine the integrity of the superannuation system. The ATO’s focus on arm’s-length terms means that the interest rate, repayment schedule, security arrangements, and every other loan condition must mirror what a commercial lender would reasonably offer.

The challenge is that family lending naturally involves trust and flexibility that commercial transactions don’t. Your sister might be willing to offer more lenient repayment terms, or your business partner might charge below-market interest rates as a favor. While these gestures seem helpful, they create compliance risks. The ATO has published extensive guidance outlining what constitutes arm’s-length terms, including safe harbour provisions that provide a compliance pathway for trustees. Meeting these standards requires formal documentation, regular reviews, and often professional advice to ensure your arrangement won’t trigger regulatory scrutiny.

How Limited Recourse Borrowing Works in Practice

At its core, a limited recourse borrowing arrangement operates through a specific structural framework designed to protect both the SMSF and the lender. When your SMSF wants to purchase a property using borrowed funds, the asset must be held in a separate trust—commonly called a holding trust or bare trust. Your SMSF becomes the beneficial owner of the asset, enjoying all the benefits like rental income and capital growth, but legal title sits with the holding trust until the loan is fully repaid.

Here’s where the “limited recourse” element becomes crucial. If your SMSF defaults on the loan, the lender’s recovery rights are restricted to the single asset held in the holding trust. They cannot pursue other SMSF assets to recover their losses. This protection is fundamental to why SMSFs are permitted to borrow at all—without it, a loan default could devastate your entire retirement savings. For example, if your SMSF borrows $500,000 to purchase a commercial property worth $650,000, and market conditions deteriorate causing a default, the lender can only claim the commercial property. Your SMSF’s share portfolio, cash reserves, and other investments remain protected.

This structural protection applies whether you’re borrowing from a commercial bank or a related party. However, the practical workings become more complex with family loans. You’ll need a written loan agreement specifying the interest rate, repayment schedule, default provisions, and the limited recourse nature of the arrangement. The holding trust must be properly established with appropriate documentation, and legal title must be correctly registered. Many trustees underestimate the administrative requirements, assuming a simple family agreement will suffice—this assumption has cost numerous SMSFs their compliant status.

Asset Acquisition Restrictions with Related Parties

Not every asset can be acquired from a related party under an LRBA, and this restriction frequently catches trustees off guard. The SIS Act generally prohibits SMSFs from acquiring assets from related parties, with specific exceptions carved out to balance investment opportunity with member protection. Understanding these exceptions is critical when your limited recourse borrowing SMSF related party arrangement involves purchasing an asset from someone connected to the fund.

The two main permitted categories are business real property and listed securities. Business real property includes commercial premises, industrial facilities, and retail spaces—but not residential property. This means your SMSF can borrow to purchase a warehouse from your family company or a medical practice building from your business trust, provided the property is used solely for business purposes and never for personal residential use. Many trustees mistakenly believe they can buy a residential investment property from their spouse using SMSF funds, but this arrangement violates the related party acquisition rules regardless of whether borrowing is involved.

Listed securities represent the second exception. Your SMSF can acquire shares or units in widely held trusts from related parties, provided the securities are listed on a recognized stock exchange and acquired at market value. This exception allows limited flexibility in restructuring family investment portfolios through superannuation, but strict market value requirements apply. The rationale behind these restrictions is preventing conflicts of interest where related parties offload underperforming or overvalued assets to SMSFs, essentially shifting investment losses onto retirement savings while benefiting the related party.

Even when acquiring permitted assets, the transaction must occur at market value. You cannot purchase business real property from your company at a “friends and family” discount, and you cannot overpay for listed securities to provide a windfall to the related party seller. Independent valuations are essential to demonstrate fair market value, and documentation must clearly establish that no preferential terms influenced the transaction. These requirements apply with equal force whether your SMSF is borrowing to fund the purchase or paying cash.

Compliance Guidelines and Safe Harbour Terms

The ATO and industry bodies have established clear guidelines for structuring compliant limited recourse borrowing SMSF related party arrangements. These guidelines provide a practical roadmap for trustees seeking to leverage related party loans while maintaining their fund’s concessional tax status. Central to these guidelines is the concept of “safe harbour” terms—specific loan conditions that, if met, provide a presumption of arm’s-length dealings.

Safe harbour terms for related party LRBAs include specific parameters around interest rates, loan terms, and documentation requirements. The interest rate must reflect commercial lending rates for similar loans, typically supported by evidence of rates offered by banks or non-bank lenders for SMSF property loans. Currently, competitive SMSF loan solutions start from 6.24% for principal and interest loans, and your related party arrangement should align with or exceed these commercial benchmarks to demonstrate arm’s-length terms. Charging your SMSF an interest rate significantly below market rates raises immediate red flags with the ATO.

Loan terms must also mirror commercial arrangements. This includes reasonable loan-to-value ratios, typically not exceeding 80% of the property value, appropriate repayment schedules reflecting the SMSF’s capacity to service debt, and security arrangements consistent with commercial lending practices. The loan agreement must be documented in writing before the borrowing occurs, with clear terms covering interest rate calculations, repayment obligations, default provisions, and the limited recourse nature of the security. Verbal agreements or informal family arrangements fail to meet compliance standards.

Ongoing compliance checks are equally important. Your SMSF must actually make loan repayments according to the agreed schedule—missed or irregular payments, even when the related party lender doesn’t mind, can indicate the arrangement isn’t genuinely arm’s-length. Interest must be calculated and paid correctly, and any variations to loan terms must be documented with justification for why the changes align with commercial practice. Many trustees establish related party LRBAs correctly but fail to maintain proper ongoing administration, creating compliance vulnerabilities that emerge during audits years later.

Risks of Non-Compliance and Governance Challenges

The consequences of getting a limited recourse borrowing SMSF related party arrangement wrong extend far beyond administrative headaches. Non-compliance can trigger the non-arm’s-length income provisions, causing investment income from the arrangement to be taxed at 45% rather than the concessional 15% rate that makes superannuation attractive. For a property generating $30,000 in annual rental income, this difference means paying $13,500 in tax instead of $4,500—a $9,000 annual penalty that compounds over the life of the investment.

More severe consequences await trustees whose arrangements are deemed to violate the borrowing restrictions or in-house asset rules. The ATO can issue penalties ranging from administrative penalties for documentation failures to significant financial penalties for more serious breaches. In extreme cases, the SMSF may lose its compliant status entirely, forcing all fund assets to be assessed at the top marginal tax rate. These aren’t theoretical risks—the ATO has successfully pursued numerous cases where related party LRBAs failed to meet arm’s-length requirements, and the financial consequences for affected trustees have been devastating.

Governance challenges represent another dimension of risk when involving family in your SMSF’s borrowing arrangements. Related party transactions create inherent conflicts of interest that must be carefully managed. When your SMSF needs to negotiate loan terms with your spouse or business partner, can you truly maintain the independence required for arm’s-length dealings? When payment difficulties arise, will family relationships pressure you to prioritize the lender over the SMSF’s interests? These conflicts aren’t easily resolved through documentation—they require ongoing vigilance and often tough decisions that strain personal relationships.

Professional advice becomes indispensable when navigating these challenges—discover how financial advisors enhance SMSF loan success. Attempting to structure a limited recourse borrowing SMSF related party arrangement without expert guidance is like performing surgery using internet instructions—the risks far outweigh any cost savings. Qualified SMSF advisors can help establish compliant loan structures, prepare appropriate documentation, conduct market value assessments, and provide ongoing compliance monitoring. Many trustees who’ve faced ATO penalties for non-compliant arrangements cite the same regret: they thought they could handle it themselves to save advisor fees, only to pay multiples more in penalties and lost tax benefits.

Strategic Considerations for SMSF Trustees

Understanding the rules is only the beginning—smart SMSF trustees must also consider whether a related party LRBA is the right strategy for their circumstances. Commercial SMSF loans from specialized lenders offer advantages that related party arrangements cannot match. Fast approvals within 1-3 business days, competitive rates starting from 6.24%, and pre-established compliance frameworks eliminate much of the uncertainty and documentation burden. When you borrow from a commercial lender, there’s no question about whether terms are arm’s-length—they clearly are.

However, related party LRBAs can offer strategic benefits in specific situations. Family lending may provide access to capital when commercial lenders decline, particularly for unique properties or circumstances outside standard lending criteria. Related party lenders might offer more flexible approaches to temporary payment difficulties, provided variations are properly documented and justified. For families implementing sophisticated wealth transfer strategies, related party LRBAs can form part of broader estate planning structures when expertly designed and maintained.

The decision requires careful analysis of your SMSF’s investment strategy, the specific property opportunity, your family’s financial dynamics, and your capacity to maintain rigorous compliance standards. At Aries Financial, we believe in empowering trustees with the knowledge and tools to make informed decisions that maximize their financial future. This means sometimes recommending commercial lending solutions over related party arrangements when the compliance risks outweigh the benefits, and other times helping structure compliant related party LRBAs when they genuinely serve the fund’s strategic objectives.

Protecting Your Retirement Investment

Limited recourse borrowing arrangements offer SMSF trustees powerful opportunities to leverage property investment for retirement wealth creation. When properly structured and maintained, they allow you to acquire high-value assets that would otherwise be beyond reach, building a diversified portfolio that supports long-term financial security. However, when related parties enter these arrangements as lenders, the compliance requirements intensify dramatically, and the margin for error shrinks to almost nothing.

The key to success lies in understanding that arm’s-length requirements aren’t bureaucratic obstacles—they’re safeguards protecting your retirement savings from arrangements that might benefit family members at the SMSF’s expense. Every element of your limited recourse borrowing SMSF related party arrangement must withstand scrutiny: the interest rate must reflect commercial terms, documentation must be comprehensive and maintained, loan conditions must be honored regardless of family relationships, and asset valuations must be independently verified. These aren’t optional refinements—they’re essential foundations for maintaining your SMSF’s concessional tax status.

At Aries Financial, our philosophy centers on integrity, expertise, and empowerment in SMSF lending. We’ve seen how related party LRBAs can both build wealth and destroy retirement plans, depending on whether trustees approach them with proper guidance and discipline. As Australia’s trusted SMSF lending specialist, we’re committed to helping trustees navigate these complex arrangements with transparency and confidence, whether that means structuring compliant related party loans or providing competitive commercial alternatives that eliminate compliance concerns.

Your superannuation represents decades of disciplined saving and strategic investment. Don’t let a well-intentioned family loan arrangement jeopardize everything you’ve built. Whether you’re considering a related party LRBA or exploring commercial SMSF lending options, the time to understand the rules and make informed decisions is before you sign the loan documents—not after the ATO audit notice arrives. Your retirement security depends on getting these decisions right, and that means working with specialists who understand both the opportunities and the obligations that limited recourse borrowing arrangements create.