When self-managed super fund (SMSF) trustees decide to invest in property using borrowed money, they enter a complex legal arrangement that trips up even experienced investors. The bare trust structure sits at the heart of this arrangement, yet it’s frequently misunderstood, incorrectly set up, or overlooked entirely. This single mistake can invalidate your entire borrowing arrangement and put your retirement savings at risk.

Let me explain what a bare trust actually is and why getting it right matters more than you think.

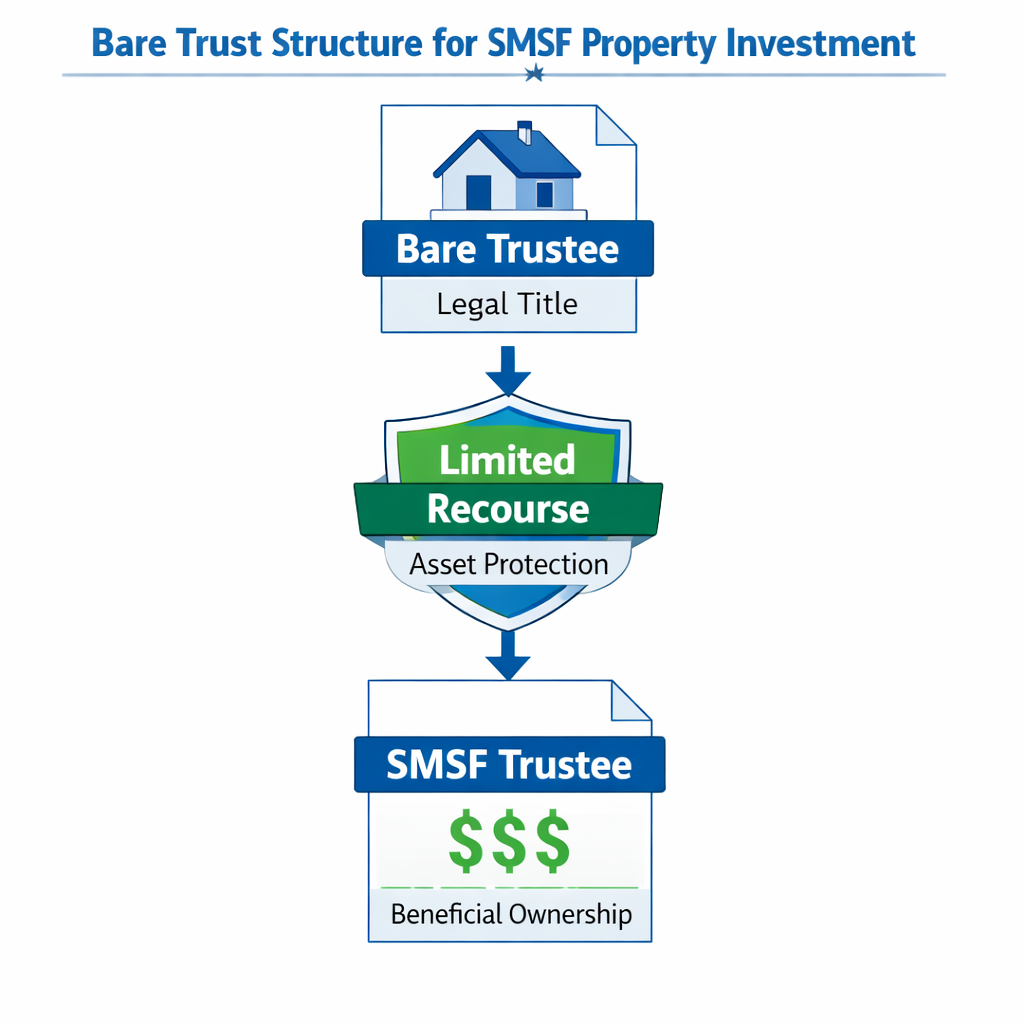

What Is a Bare Trust and Why Does It Matter for SMSF Borrowing?

A bare trust is a legal structure specifically designed to hold property title during an SMSF loan arrangement. When your super fund borrows money to buy property, superannuation law doesn’t allow the SMSF to hold the property title directly while debt exists against it. Instead, a bare trust steps in as an intermediary.

Here’s how it works: The bare trustee holds the legal title to the property, while your SMSF retains beneficial ownership. Think of it like this—the bare trustee’s name appears on the property deed, but your super fund enjoys all the benefits. Your SMSF collects the rental income, claims the tax deductions, and ultimately owns the asset once the loan is repaid.

This separation exists for one critical reason: asset protection. Under a Limited Recourse Borrowing Arrangement (LRBA), if something goes wrong and your SMSF can’t repay the loan, the lender’s recourse is limited to only the property held in the bare trust. Your other super fund assets—shares, cash, other properties—remain protected. Without this structure, a property investment gone wrong could wipe out your entire retirement savings.

The bare trust isn’t optional. It’s a fundamental compliance requirement under sections 67A and 67B of the Superannuation Industry (Supervision) Act 1993. Miss this step, and your SMSF borrowing arrangement fails to meet legal requirements from day one.

Understanding the Structure and Process

Setting up a bare trust for SMSF borrowing involves several key players and precise legal steps. Getting the structure right from the start saves you from costly compliance issues later.

The SMSF Trustee’s Role

Your SMSF trustee—whether individual trustees or a corporate trustee—remains responsible for the fund’s investment strategy and loan repayments. The SMSF trustee enters into the loan agreement with the lender, typically starting at competitive rates like 5.99% for principal and interest loans. The trustee manages the property investment, collects rental income into the super fund, and ensures loan repayments are made from fund resources.

The Bare Trustee’s Function

The bare trustee is a separate legal entity that holds the property title during the loan period. This can be an individual or a company, but here’s the critical part: the bare trustee cannot be the same entity as your SMSF trustee. Using the same individual or corporate trustee for both roles is a clear breach of LRBA rules and invalidates your entire borrowing arrangement.

The bare trustee has minimal discretion. They hold legal title but cannot make decisions about the property without direction from the SMSF trustee. They’re essentially a “bare” legal owner—hence the name—with no active management role.

The LRBA Framework

The Limited Recourse Borrowing Arrangement ties everything together. Under an LRBA, your SMSF borrows money to acquire a single acquirable asset—the property. The loan agreement must specify that the lender’s rights are limited to the asset held in the bare trust. If your SMSF defaults, the lender cannot pursue other fund assets.

The loan must be conducted on arm’s length terms. This means commercial interest rates, realistic repayment schedules, and proper security arrangements. If you’re borrowing from a related party—say, your own company—the terms must mirror what an independent bank would offer. The ATO scrutinizes related party loans closely, so documentation must be impeccable.

Key Setup Requirements You Cannot Skip

Successfully establishing a bare trust for SMSF borrowing demands attention to specific compliance requirements. Miss any of these steps, and your structure may fail ATO scrutiny.

Update Your SMSF Trust Deed

Before you do anything else, check your SMSF trust deed. Not all trust deeds include provisions allowing borrowing or establishing bare trusts. If yours is outdated or restrictive, you’ll need to update it. This legal document governs what your fund can and cannot do, so it must explicitly permit LRBAs.

Appoint an Appropriate Bare Trustee

Choose your bare trustee carefully. Many SMSF trustees set up a separate company to act as bare trustee—this creates a clear legal separation and professional structure. Some use a trusted individual, but remember: this person or entity holds legal title to potentially millions of dollars in property. They need to be reliable, understand their limited role, and remain available throughout the loan term.

Crucially, the bare trustee must be independent from the SMSF trustee structure. This separation isn’t just a technicality—it’s a fundamental requirement that protects the integrity of the LRBA framework.

Draft the Bare Trust Deed

The bare trust deed is the legal document that establishes the bare trust and defines the relationship between the SMSF trustee and bare trustee. This deed must clearly state that:

- The bare trustee holds legal title only

- The SMSF retains beneficial ownership

- The bare trustee acts solely on direction from the SMSF trustee

- The arrangement exists to facilitate the LRBA

Many property investors make the mistake of using generic trust deed templates. SMSF lending operates under specific superannuation law requirements. Your bare trust deed must align with ATO guidelines, so invest in proper legal drafting.

Obtain Independent Property Valuation

The ATO requires that property purchased by an SMSF be acquired at market value. This means getting an independent valuation from a qualified valuer before settlement. The valuation protects your fund from allegations of preferential treatment, especially if purchasing from a related party.

Arrange Appropriate Insurance

Property insurance becomes slightly more complex with a bare trust structure. The property is legally owned by the bare trustee but beneficially owned by the SMSF. Insurance policies must reflect this arrangement, naming both parties appropriately. Many standard insurance policies don’t account for bare trust structures, so work with insurers experienced in SMSF property investment.

Compliance and Regulatory Considerations

LRBAs sit under intense ATO scrutiny, and for good reason—they represent significant borrowing within the superannuation system. Understanding compliance requirements helps you avoid the pitfalls that catch many property investors.

The Sole Purpose Test

Every SMSF investment must satisfy the sole purpose test: providing retirement benefits to fund members. When you borrow to buy property through a bare trust, the investment must align with your fund’s retirement goals, not provide current-day benefits to members or their relatives.

This means you cannot:

- Live in the property yourself

- Allow family members to live there rent-free or at below-market rent

- Use the property for personal purposes

Even temporarily staying at the property during a holiday violates the sole purpose test. The property must be maintained purely as an investment asset for retirement benefit purposes.

Avoiding Prohibited Arrangements

Superannuation law prohibits certain arrangements that could advantage fund members or related parties improperly. Common prohibited arrangements include:

- Purchasing the property from a related party (with limited exceptions for business real property)

- Arranging loans on non-commercial terms

- Providing personal guarantees that extend liability beyond the limited recourse structure

The ATO has specific safe harbour provisions for certain related party loans, but these come with strict documentation and compliance requirements.

Tax Implications to Consider

Stamp duty applies when property is transferred into the bare trust structure. Each state has different stamp duty rates and concessions, so factor these costs into your investment calculations.

Capital gains tax (CGT) becomes relevant when your SMSF eventually sells the property. If held for more than 12 months, your super fund receives a 33.33% CGT discount. Once your fund enters pension phase, capital gains can potentially be tax-free. However, the timing of selling relative to your fund’s tax status significantly impacts your after-tax return.

Income tax on rental earnings is typically 15% in accumulation phase or 0% in pension phase. Your SMSF must lodge annual tax returns showing rental income and loan interest deductions.

Practical Advantages of the Bare Trust Structure

Despite its complexity, the bare trust structure enables powerful wealth-building opportunities for SMSF trustees who understand how to use it properly.

Property Exposure with Gearing

The bare trust structure allows your super fund to leverage into property markets that might otherwise remain out of reach. If your SMSF has $200,000 in cash, you’re limited to properties at that price point. But with an LRBA, you might borrow an additional $400,000, accessing $600,000 worth of property. The gearing amplifies your exposure to property market growth while building equity through loan repayments funded by rental income.

At Aries Financial, we’ve seen SMSF trustees use competitive lending rates starting from 5.99% to strategically build property portfolios within their super funds. This approach, when managed properly, accelerates retirement wealth accumulation while maintaining tax efficiency.

Clear Liability Boundaries

The limited recourse feature provides genuine peace of mind. Your property investment carries risk—rental markets fluctuate, properties can have issues, and economic conditions change. If your property investment fails and your SMSF cannot continue loan repayments, the lender’s claim stops at the property held in the bare trust.

Your other super fund assets—perhaps accumulated shares, managed funds, or business real property—remain protected. This ring-fencing of liability means a single poor property decision doesn’t destroy your entire retirement strategy.

Compliance Framework

While complex, the bare trust structure provides a clear compliance framework that protects your SMSF from regulatory issues. When set up correctly with proper legal documentation, the structure demonstrates to the ATO that you’re operating within permitted boundaries. This clarity matters during audits and helps your SMSF maintain its complying status.

Practical Risks and Pitfalls

Understanding the advantages means nothing if you fall into common traps. These risks have cost many property investors dearly.

Complexity and Setup Costs

Establishing a bare trust isn’t cheap or simple. You’ll need:

- Legal fees for the bare trust deed ($1,500-$3,000)

- Costs for setting up a corporate bare trustee if required ($500-$1,000)

- Professional advice from SMSF specialists ($2,000-$5,000)

- Property valuation ($500-$1,500)

- Stamp duty on property purchase (varies by state)

These upfront costs can easily reach $10,000 or more before you even settle on the property. Many investors underestimate these expenses, finding their SMSF doesn’t have sufficient cash reserves to cover both settlement and setup costs.

Compliance Risks

The bare trust structure must comply with numerous technical requirements. Common compliance failures include:

- Using the same trustee for both SMSF and bare trust

- Failing to maintain arm’s length terms on related party loans

- Inadequate documentation of the bare trust arrangement

- Property usage that breaches the sole purpose test

Each of these failures can result in the SMSF losing its complying status, triggering significant tax penalties. Your fund’s assets could be taxed at the top marginal rate rather than the concessional 15% super fund rate—a potentially devastating outcome.

Ongoing Management Burden

Once established, the bare trust structure requires ongoing administration. Your SMSF annual audit must verify that the LRBA continues to comply with superannuation law. You’ll need to:

- Maintain separate records for the bare trust

- Ensure loan repayments align with the loan agreement

- Keep documentation proving arm’s length dealings

- Lodge property-related tax schedules with your SMSF return

This administrative burden continues for the entire loan term, potentially decades. Many trustees underestimate the time and attention required.

Tax Charges on Structure Changes

If you decide to refinance the loan, change the bare trustee, or alter the arrangement, you may trigger additional stamp duty charges. Some states treat changes to the bare trust structure as property transfers, leading to unexpected tax bills. Before making any structural changes, seek specific tax advice on the implications.

Your Bare Trust Implementation Checklist

If you’re considering a bare trust for SMSF property investment, follow this step-by-step checklist to ensure proper setup:

Step 1: Verify Investment Strategy Alignment

Confirm that property investment aligns with your SMSF’s documented investment strategy, considering risk tolerance, diversification, and retirement timeframes.

Step 2: Check and Update Trust Deed

Review your SMSF trust deed to ensure it permits borrowing and bare trust arrangements. Update if necessary.

Step 3: Obtain Lender Pre-Approval

Secure pre-approval for your SMSF loan, confirming interest rates (starting from 5.99% PI), loan terms, and lending criteria. Fast approvals within 1-3 business days are available with specialist SMSF lenders like Aries Financial.

Step 4: Appoint Separate Bare Trustee

Establish a corporate trustee company or appoint an appropriate individual as bare trustee, ensuring complete independence from your SMSF trustee structure.

Step 5: Draft Bare Trust Deed

Engage experienced legal professionals to draft a compliant bare trust deed that meets ATO requirements and clearly establishes the relationship between SMSF trustee and bare trustee.

Step 6: Obtain Property Valuation

Commission an independent property valuation from a qualified valuer to establish market value and satisfy ATO requirements.

Step 7: Finalize Loan Documentation

Execute the loan agreement, ensuring all terms are documented in writing and comply with arm’s length requirements.

Step 8: Complete Property Settlement

Settle the property purchase with legal title transferring to the bare trustee while beneficial ownership remains with the SMSF.

Step 9: Arrange Insurance

Establish building and contents insurance that appropriately recognizes the bare trust structure.

Step 10: Implement Ongoing Compliance

Set up systems for loan repayment tracking, rental income recording, and annual audit preparation to maintain compliance throughout the loan term.

Essential Terms Explained

Understanding these key terms helps you navigate bare trust arrangements with confidence:

Bare Trust: A legal structure where the trustee holds legal title to property while another party (the SMSF) retains full beneficial ownership. The bare trustee acts purely on direction from the beneficial owner with no independent discretion.

Limited Recourse Borrowing Arrangement (LRBA): A specific borrowing structure permitted under superannuation law where the lender’s rights are limited to the asset held in the bare trust. Other SMSF assets are protected from the lender’s claims.

Beneficial Ownership vs Legal Title: Beneficial ownership means you enjoy all the rights, income, and capital gains from the property. Legal title is the name appearing on the property deed. In a bare trust, these are split—the bare trustee holds legal title while the SMSF retains beneficial ownership.

Sole Purpose Test: The fundamental requirement that all SMSF activities must be conducted solely to provide retirement benefits to fund members. Property investments must serve retirement purposes, not provide current-day benefits.

Safe Harbour Provisions: Specific ATO guidelines that, when followed precisely, provide certainty that a related party loan arrangement complies with arm’s length requirements. These include maximum loan-to-value ratios and minimum interest rates.

Getting your bare trust structure right matters profoundly for your retirement wealth strategy. The structure enables powerful wealth-building through property investment while protecting your broader super fund assets. But success requires precise legal setup, ongoing compliance attention, and professional guidance from specialists who understand SMSF lending inside and out. When established correctly and managed properly, a bare trust structure becomes a cornerstone of strategic retirement wealth accumulation through property investment.