When Sarah, a successful business owner in her late 40s, decided to take control of her retirement savings through a Self-Managed Super Fund, she quickly discovered that property investment within her SMSF could amplify her wealth-building strategy. But there was a challenge: her fund didn’t have enough cash to purchase the commercial property she’d identified. That’s when her financial advisor introduced her to a Limited Recourse Borrowing Arrangement—a specialized lending structure that would allow her SMSF to borrow money while protecting her other retirement assets.

Sarah’s story reflects the experience of thousands of Australian SMSF trustees who are exploring property investment through their superannuation funds. Understanding the limited recourse borrowing arrangement definition isn’t just about grasping technical jargon—it’s about recognizing both the opportunity and the responsibility that comes with leveraging your retirement savings.

Understanding the Core Structure of Limited Recourse Borrowing Arrangements

At its heart, a Limited Recourse Borrowing Arrangement (LRBA) is a specific borrowing structure that allows your Self-Managed Super Fund to purchase an asset—typically property—using borrowed funds while limiting the lender’s claim to only that specific asset. This “limited recourse” feature is the defining characteristic that separates LRBAs from traditional property loans.

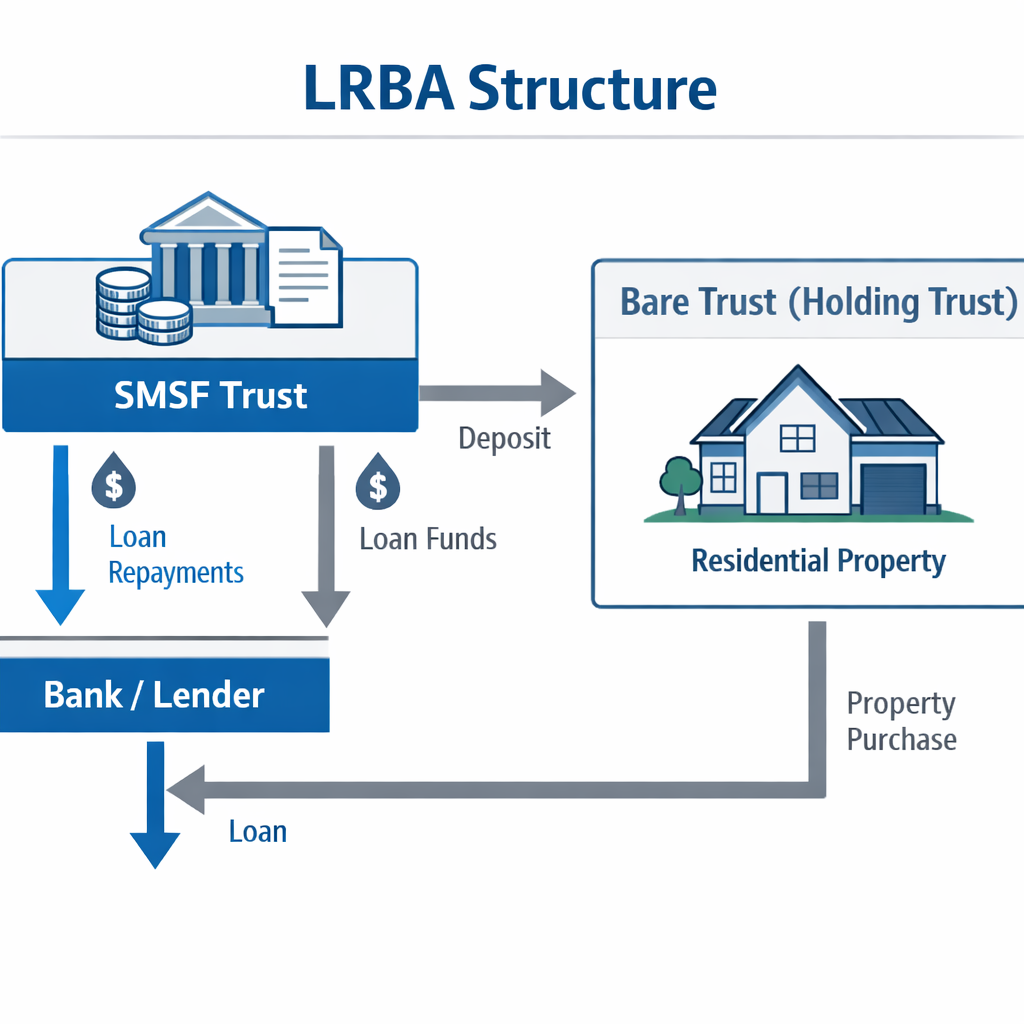

The structure involves two distinct trusts working in tandem. First, there’s your SMSF itself, which acts as the beneficial owner of the asset. Second, there’s a separate holding trust—often called a bare trust or custodian trust—which legally holds the property until the loan is fully repaid. Your SMSF borrows money from a lender, and those funds are used to purchase a single acquirable asset that’s held in the separate trust.

This two-trust setup serves a crucial protective function. If your SMSF defaults on the loan, the lender’s recourse is limited to the asset held in the holding trust. They cannot pursue other assets within your SMSF or your personal assets outside the fund. This risk containment feature makes LRBAs an attractive option for trustees who want to leverage their retirement savings without exposing their entire portfolio to lending risk.

The “single acquirable asset” requirement is another fundamental element of the limited recourse borrowing arrangement definition. Your SMSF can only borrow to purchase one asset at a time under each LRBA. That asset must be clearly identifiable and cannot be changed or substituted while the loan remains outstanding. In practical terms, this means you could borrow to buy a residential property at 123 Smith Street, but you couldn’t use that same borrowing arrangement to purchase multiple properties or to swap the original property for a different one mid-loan.

The Legal Framework: Navigating Australian Superannuation Laws

The ability to use LRBAs stems from Section 67A of the Superannuation Industry (Supervision) Act 1993, which carved out a specific exception to the general prohibition on SMSF borrowing. Before 2007, SMSFs were essentially prohibited from borrowing money. The introduction of Section 67A created a regulated pathway for strategic borrowing, but it came with strict compliance requirements that trustees must understand and follow.

Australian superannuation laws impose several non-negotiable conditions on LRBAs. The borrowed money must be used exclusively to acquire the asset—you cannot use loan funds to improve or renovate the property. Any improvements must be funded from the SMSF’s existing cash reserves. The asset must be held on trust separate from the SMSF until the loan is fully repaid. And critically, the lender’s rights if the SMSF defaults must be limited to the asset held in the holding trust.

The in-house asset rules present another compliance consideration that catches many trustees off guard. Generally, your SMSF cannot hold more than 5% of its total assets as in-house assets—investments in related parties or related trusts. If your LRBA involves lending from a related party (such as yourself, a family member, or a related company), you must ensure the arrangement doesn’t breach these rules. The consequences of non-compliance can be severe, including penalties and potential disqualification as a trustee.

Related-party lending deserves special attention in the context of LRBAs. While it’s legally permissible for your SMSF to borrow from yourself or a related party, the arrangement must be conducted on commercial terms. This means the interest rate must be comparable to what an arm’s-length lender would charge, the loan must be properly documented with a formal loan agreement, and repayments must be made as scheduled. The Australian Taxation Office scrutinizes related-party LRBAs closely, and any arrangement that appears to be a disguised benefit payment or lacks commercial substance will attract regulatory attention.

At Aries Financial, we emphasize that compliance isn’t just a box-ticking exercise—it’s the foundation of protecting your retirement assets. We’ve seen trustees lose their concessional tax treatment or face significant penalties because they didn’t understand the compliance requirements before establishing their LRBA. This is why working with specialists who understand both superannuation law and property lending is not optional—it’s essential.

How LRBAs Work in Practice: The Typical Loan Flow

Let’s walk through how a typical LRBA unfolds for property investment. Imagine your SMSF has $200,000 in cash, and you’ve identified a residential investment property worth $500,000. Without borrowing, this property would be out of reach. An LRBA changes that equation.

First, you establish a separate holding trust with a bare trustee (often a corporate trustee created specifically for this purpose). Your SMSF then enters into a loan agreement with a lender—this could be a specialized non-bank lender like Aries Financial, which focuses exclusively on SMSF lending, or it could be a traditional bank that offers SMSF loans. With competitive rates starting from 5.99% on principal and interest loans, specialist lenders often provide more favorable terms and faster approval times than traditional banks.

The lender provides $300,000 to the holding trust, which combines this with your SMSF’s $200,000 contribution to purchase the property. Legal title to the property sits with the holding trust, but your SMSF has beneficial ownership—meaning your fund enjoys all the benefits of ownership, including rental income and capital appreciation, while the holding trust simply holds legal title as security for the lender.

Your SMSF makes regular loan repayments to the lender using the property’s rental income and, if necessary, other fund income or contributions. All rental income flows to your SMSF, and all expenses related to the property—rates, insurance, maintenance, and loan repayments—are paid by your SMSF. Once the loan is fully repaid, legal title transfers from the holding trust to your SMSF, and the two-trust structure dissolves.

The types of assets commonly financed through LRBAs extend beyond just residential property. Commercial property, such as office spaces, retail shops, or industrial units, represents a significant portion of LRBA-funded acquisitions. Some trustees use LRBAs to purchase the business premises from which they operate their company, allowing them to pay rent to their own SMSF rather than to an external landlord. Commercial property through SMSF loans offers both rental income and capital growth potential. Residential property remains popular due to its accessibility, liquidity, and the potential for steady rental returns combined with long-term capital growth.

The benefits of this structure are compelling. An LRBA gives your SMSF access to high-value investments that would otherwise be unaffordable, allowing you to leverage your existing capital to control a larger asset base. Property appreciation occurs within the tax-advantaged superannuation environment—taxed at just 15% during accumulation phase or potentially tax-free in pension phase. Rental income provides cash flow to service the loan and contribute to your retirement savings. And the limited recourse feature protects your other SMSF assets from lending risk.

The Risks and Caveats Every Trustee Must Consider

However, LRBAs are not without their challenges and risks. The complexity of managing a two-trust structure with strict compliance requirements means these arrangements demand more attention and expertise than straightforward property ownership. You’re not just managing a property investment—you’re managing a sophisticated financial structure governed by superannuation law.

The costs associated with LRBAs extend beyond the interest rate on the loan. You’ll face establishment fees for setting up the holding trust, potentially higher interest rates compared to standard home loans (since lenders view SMSF lending as higher risk), ongoing compliance costs for independent audits, and legal fees for ensuring all documentation meets regulatory standards. When Sarah from our opening example set up her LRBA, she discovered that the total establishment costs exceeded $5,000, and her annual audit fees increased by nearly $1,000 due to the additional complexity.

Compliance risks loom large with LRBAs. Any breach of the strict conditions—using borrowed funds for improvements, failing to maintain the asset in the holding trust, allowing the loan terms to become non-commercial—can result in the entire arrangement being deemed non-compliant. The ATO’s rules for entering an LRBA outline these compliance requirements in detail. The consequences cascade quickly: the loan becomes an illegal early access to superannuation benefits, triggering penalty taxes of up to 93% of the loan value, potential disqualification as a trustee, and loss of the concessional tax treatment that makes superannuation attractive.

Liquidity presents another significant consideration. Property is inherently illiquid, meaning you cannot quickly convert it to cash if your SMSF needs to pay member benefits or cover unexpected expenses. If a member wants to exit the fund or reaches retirement and requests a benefit payment, you must ensure sufficient liquidity to meet that obligation without being forced into a distressed sale of the property. Many trustees underestimate this risk, assuming rental income will always cover expenses and loan repayments. But vacancies happen, maintenance costs spike unexpectedly, and interest rates can rise—all of which strain your SMSF’s cash flow.

The concentration risk of holding a single, large asset within your SMSF portfolio also warrants consideration. If property values decline in your specific location or property type, your SMSF could experience significant capital losses. This is why investment strategy documentation must justify how the LRBA-funded property fits within your fund’s overall investment approach and risk tolerance. Relying too heavily on a single property through an LRBA could expose the fund to concentrated risk that contradicts your documented investment strategy.

Ongoing governance requirements mean LRBAs demand sustained attention. Every year, your independent auditor will scrutinize the arrangement to ensure compliance. You must maintain detailed records of all transactions, ensure loan repayments are made on schedule, and document that any related-party arrangements remain on commercial terms. At Aries Financial, we’ve observed that trustees who succeed with LRBAs treat compliance as an ongoing commitment, not a one-time setup task.

Practical Compliance Steps and Considerations for SMSF Trustees

If you’re considering an LRBA for your SMSF, certain practical steps will help ensure compliance and protect your retirement assets. First and foremost, verify that your SMSF trust deed specifically permits borrowing. Not all trust deeds include the necessary provisions, and attempting to establish an LRBA without proper deed authority creates immediate compliance issues. If your deed doesn’t permit borrowing, you’ll need to update it before proceeding.

Working with experienced advisors cannot be overstated. The interplay between superannuation law, property law, and lending regulations creates complexity that generalist advisors may not fully understand. Specialist SMSF lawyers can structure the holding trust correctly and draft loan agreements that meet regulatory requirements. Specialist SMSF auditors understand what documentation and evidence they need to verify compliance. And specialist SMSF lenders, like Aries Financial, understand the unique requirements and can provide loan approvals within 1-3 business days rather than the weeks traditional banks often require.

Proper valuation of the asset at acquisition is another critical compliance step. Your SMSF must acquire the asset at market value—neither overpaying to benefit a related party seller nor underpaying to gain an unfair advantage. Independent valuations provide evidence that the transaction occurred on arm’s-length terms, protecting trustees from allegations of non-compliance or providing illegal benefits to members.

Record maintenance becomes paramount with LRBAs. You must maintain copies of all loan documents, the holding trust deed, evidence of market value at acquisition, records of all loan repayments, documentation of any improvements funded from SMSF cash reserves, and evidence that rental income and expenses are properly allocated. These records serve as your defense if your arrangement is ever questioned during an audit or ATO review.

Consider your exit strategy before establishing the LRBA. How will your SMSF repay the loan? What happens if a member wants to access their benefits before the loan is repaid? What’s your plan if the property’s value declines or rental income falls short of expectations? Trustees who answer these questions upfront are better positioned to navigate challenges that inevitably arise over the life of a long-term property investment.

The investment strategy must specifically address the LRBA and how it aligns with your fund’s objectives, risk tolerance, and liquidity needs. Your strategy should explain why borrowing to purchase this particular property serves your members’ retirement interests, how you’ll manage the cash flow requirements, and what diversification exists beyond this single asset. For comprehensive guidance on SMSF borrowing and property investing, trustees should consult multiple authoritative sources. A well-documented investment strategy not only ensures compliance—it provides a roadmap for making informed decisions throughout the life of the LRBA.

Quick Takeaway: Power Paired with Responsibility

A Limited Recourse Borrowing Arrangement represents one of the most powerful wealth-building tools available to SMSF trustees. It allows you to leverage your retirement savings to acquire high-value assets, potentially accelerating your path to a comfortable retirement. The protective limited recourse structure means your other SMSF assets remain insulated from lending risk, and the tax-advantaged superannuation environment amplifies investment returns compared to holding property outside super.

But with this power comes significant responsibility. The compliance requirements are strict, the costs are real, and the ongoing management demands sustained attention. Trustees who succeed with LRBAs are those who understand the limited recourse borrowing arrangement definition not as a technical concept, but as a serious commitment to proper governance, expert advice, and disciplined execution.

At Aries Financial, our philosophy centers on integrity, expertise, and empowerment. We believe in simplifying SMSF lending while maintaining the highest standards of compliance and transparency. Our exclusive focus on SMSF financing means we understand the nuances that generalist lenders miss. We’re not just providing a loan—we’re partnering with you to maximize your retirement investment potential while ensuring you meet every regulatory requirement.

Before you establish an LRBA, ask yourself: Do I fully understand the compliance obligations? Have I assembled the right team of advisors? Does my investment strategy justify this borrowing? Am I prepared for the ongoing governance requirements? If you can confidently answer yes to these questions, an LRBA might be the strategic tool that transforms your retirement savings. If doubts remain, take the time to educate yourself and seek specialized advice. Your retirement security deserves nothing less than informed, deliberate decision-making.