Imagine turning your superannuation into a property empire. Not the reckless, late-night-infomercial kind of empire, but a carefully structured, compliance-friendly wealth-building machine that works while you sleep. That’s the promise of borrowing within your Self-Managed Super Fund (SMSF), and it’s not as complicated as it sounds—though it’s certainly not as simple as buying your first pair of joggers online either.

At Aries Financial, we’ve helped countless Australians navigate the strategic maze of SMSF property investment. With loan solutions starting from 5.99% PI and approvals that typically take just 1-3 business days, we’ve streamlined what many perceive as an impossibly complex process. But before we dive into the timeline, let’s address the elephant in the room: Yes, SMSFs can borrow money. No, it’s not some legal loophole that’ll land you in hot water with the Australian Taxation Office. It’s called a Limited Recourse Borrowing Arrangement (LRBA), and when structured correctly, it’s one of the most powerful wealth-building tools in your retirement arsenal.

The strategic benefits are compelling. You’re leveraging your super to purchase investment property, potentially accelerating your retirement wealth while maintaining the tax advantages that make SMSFs so attractive in the first place. Property values appreciate within a concessional tax environment, rental income flows back into your fund, and you’re building equity using borrowed funds. It’s financial judo—using leverage to amplify your position without overstretching your current resources.

Understanding the LRBA Structure: The Bare Bones (and the Bare Trust)

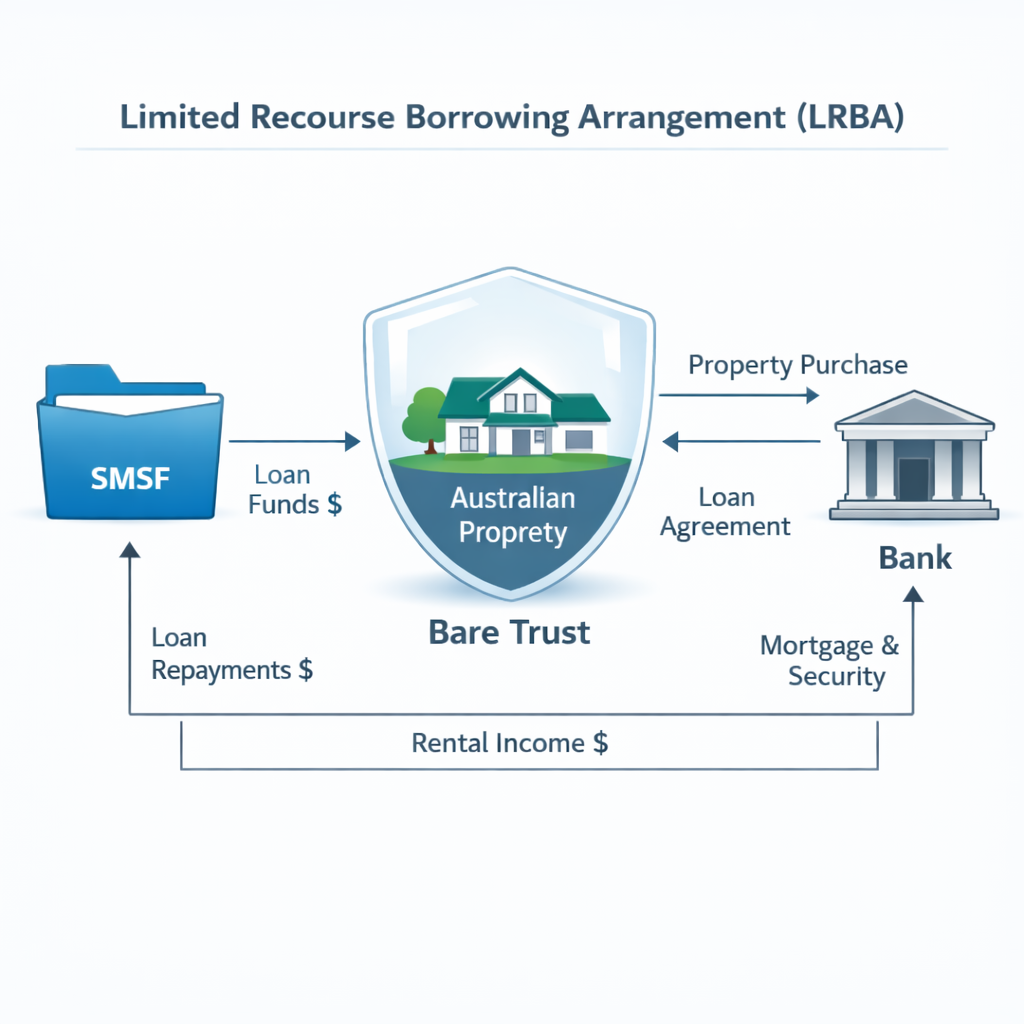

Let’s talk structure, because getting this right is non-negotiable. An LRBA isn’t just any old loan—it’s a carefully choreographed arrangement involving three key players: your SMSF, a bare trust (also called a holding trust), and a lender.

Here’s how it works: Your SMSF borrows money to purchase a property, but that property doesn’t sit directly in your SMSF’s name. Instead, it’s held in a bare trust, with your SMSF as the beneficial owner. Think of the bare trust as a protective wrapper—it holds legal title to the property on behalf of your SMSF. This structure creates the “limited recourse” feature, which is the entire point of the exercise.

The limited recourse aspect means that if things go south—if you default on the loan—the lender’s claim is limited to the asset purchased with that specific loan. They can’t raid your other SMSF assets. Your vintage share portfolio? Safe. Your other investment properties? Untouchable. Only the property securing that particular LRBA is at risk. It’s like a financial firewall, protecting your broader retirement savings from a single investment going sideways.

But here’s where compliance becomes critical, and why partnering with specialists like Aries Financial matters. The asset must be a “single acquirable asset” under superannuation law. You can’t buy a duplex and treat it as two separate investments. You can’t purchase a property and then subdivide it within the trust arrangement. And you absolutely cannot use the borrowed funds for renovations or improvements—only acquisition costs are permitted. Break these rules, and you’re not just facing penalties; you risk the entire arrangement being deemed non-compliant, potentially triggering massive tax consequences.

At Aries Financial, integrity isn’t just a buzzword we throw around in marketing materials. We’ve built our reputation on ensuring every LRBA structure meets the stringent requirements of the Superannuation Industry (Supervision) Act 1993. We don’t just process loans; we educate our clients on maintaining compliance throughout the life of the arrangement.

The 7-Phase Timeline: From Strategic Planning to Keys in Hand

Now for the practical roadmap. Buying property through your SMSF isn’t a weekend project—it’s a multi-phase journey that requires patience, planning, and professional guidance.

Phase 1: Strategic Planning and Investment Strategy (Weeks 1-2)

Before you even think about browsing property listings, you need to document your investment strategy. The Australian Taxation Office requires every SMSF to maintain a written investment strategy that outlines how your fund’s investments align with your retirement objectives. This isn’t bureaucratic box-ticking; it’s forcing you to think critically about whether property investment makes sense for your specific circumstances.

During this phase, you’ll assess your SMSF’s current balance, contribution capacity, and cash flow requirements. Can your fund service a loan? Do you have sufficient liquidity to cover the deposit, stamp duty, and ongoing expenses? Will this investment compromise your ability to pay member benefits when required? These aren’t hypothetical questions—they’re compliance requirements that could make or break your LRBA.

Here’s where the process gets real: You’ll need to engage professionals. An experienced SMSF accountant or advisor should review your fund’s structure, ensure your trust deed permits borrowing (not all do), and confirm your fund meets the compliance requirements for an LRBA. This phase typically costs between $2,000 and $5,000, depending on complexity, but it’s money well spent. As we say at Aries Financial, the cheapest professional advice is the advice that prevents you from making expensive mistakes.

Phase 2: Loan Pre-Approval (Weeks 3-4)

Armed with a solid investment strategy, you’re ready to approach lenders. This is where Aries Financial’s expertise truly shines. Our streamlined pre-approval process typically takes 1-3 business days, giving you the confidence to make offers on properties knowing exactly what you can borrow.

SMSF lending differs significantly from residential home loans. Lenders assess serviceability based on rental income projections, not your personal income. Most lenders require the property to generate sufficient rental yield to cover interest payments, typically looking for an interest coverage ratio of 1.4 times or higher. With residential SMSF loans available up to 90% Loan-to-Value Ratio (LVR) and commercial properties up to 80% LVR, Aries Financial provides options that maximize your borrowing capacity while maintaining conservative risk management.

During pre-approval, you’ll need to provide your SMSF trust deed, recent financial statements, investment strategy, and details about fund members. The lender will assess your fund’s ability to service the loan—not just today, but under stressed interest rate scenarios. This conservative approach protects both you and the lender, ensuring the arrangement remains sustainable even if market conditions deteriorate.

Phase 3: Property Search and Due Diligence (Weeks 5-8)

With pre-approval secured, the fun part begins—property hunting. But don’t let excitement override due diligence. Every property you consider must be acquired on commercial terms at market value. The ATO takes a dim view of SMSFs purchasing property from related parties or paying over-market prices.

This phase requires professional property valuations, building and pest inspections, and thorough research into rental yields and capital growth potential. Remember, this isn’t about finding your dream home; it’s about acquiring an investment asset that aligns with your retirement objectives. The property must stack up financially—generating sufficient rental income to cover loan repayments and ongoing expenses while delivering long-term capital appreciation.

Many investors make the mistake of falling in love with a property emotionally rather than evaluating it rationally. Your SMSF doesn’t care about the charming period features or the stunning water views—it cares about returns, serviceability, and compliance. This is where having a clear investment strategy proves invaluable, keeping you focused on properties that meet your fund’s objectives.

Phase 4: Formal Loan Application and Bare Trust Setup (Weeks 9-10)

Once you’ve identified a suitable property and made an offer, the formal application process begins. You’ll need to establish the bare trust arrangement before settlement, which involves engaging a legal professional to draft the trust deed. This document must precisely specify the asset being acquired and correctly identify your SMSF as the beneficial owner.

The bare trust deed is not a DIY job. Template documents downloaded from the internet rarely meet the specific requirements of SMSF LRBAs, and errors in the trust structure can invalidate the entire arrangement. Professional legal fees for establishing a bare trust typically range from $800 to $2,000, depending on the complexity and jurisdiction.

Simultaneously, you’ll submit your formal loan application to Aries Financial, providing updated financial information, the property contract, and confirmation of the bare trust structure. Our experienced lending team reviews every detail, ensuring compliance with both banking requirements and SMSF legislation. We’re not just processing paperwork—we’re partnering with you to structure an arrangement that protects your retirement savings while maximizing investment potential.

Phase 5: Loan Approval and Contract Exchange (Week 11)

With the formal application assessed, loan approval typically follows within days. Aries Financial’s specialized focus on SMSF lending means we understand the unique requirements of these transactions, avoiding the delays and confusion that plague investors working with mainstream lenders unfamiliar with LRBA structures.

Upon approval, you’ll exchange contracts on the property, paying the deposit from your SMSF’s available funds. This is a critical compliance point: The deposit must come from your SMSF, not from personal funds or related party loans. Many investors trip up here, inadvertently creating compliance issues by trying to “help” their SMSF with personal contributions outside the contribution caps.

During this phase, you’ll also arrange insurance—both for the property itself and, importantly, insurance protecting the bare trust arrangement. The bare trust (as the legal owner) must be listed on property insurance policies, while your SMSF (as the beneficial owner) should also be noted. Get this wrong, and you could face a nightmarish insurance claim situation.

Phase 6: Settlement Preparation (Weeks 12-13)

The final stretch involves coordinating multiple parties: your SMSF trustee, the lender, your solicitor or conveyancer, the bare trustee, and the vendor’s representatives. Settlement statements must be reviewed meticulously, ensuring all costs are properly allocated and that funds flow correctly through the various accounts.

Your SMSF will need sufficient cash reserves to cover settlement costs including stamp duty, legal fees, and loan establishment fees. These expenses can be substantial—stamp duty alone typically ranges from 4% to 6% of the property value in most states. Missing this cash flow requirement creates settlement risks that could derail the entire transaction.

Aries Financial’s role during this phase is ensuring the loan funds are ready to disburse on settlement day. Our team coordinates with solicitors and conveyancers, confirming all documentation is correct and all conditions have been satisfied. We’ve seen enough settlement dramas to know that proactive communication and meticulous attention to detail are what separate smooth settlements from costly disasters.

Phase 7: Settlement and Post-Settlement Administration (Week 14 onward)

Settlement day arrives, and if everything has been planned correctly, it’s anticlimactic in the best possible way. Ownership transfers to the bare trust, loan funds are released, and your SMSF officially becomes the beneficial owner of an investment property.

But the journey doesn’t end at settlement. Post-settlement compliance is an ongoing responsibility. Your SMSF must maintain adequate records of all transactions, ensure rental income is deposited directly into the fund’s bank account, and pay all expenses from the fund. The property must never be occupied by fund members or related parties—doing so would violate the sole purpose test and create serious compliance issues.

Quarterly loan repayments must be made on time, your SMSF’s annual financial statements must accurately reflect the LRBA structure, and your annual audit must confirm ongoing compliance. This administrative burden is real, but it’s manageable with proper systems and professional support.

Financial Considerations: Counting the Real Costs

Let’s talk dollars and sense (yes, both spellings are intentional). SMSF property investment through borrowing isn’t cheap to establish, and understanding the full cost structure prevents nasty surprises.

Upfront establishment costs typically include:

- SMSF advice and investment strategy updates: $2,000–$5,000

- Bare trust establishment: $800–$2,000

- Property valuation: $400–$800

- Legal fees and conveyancing: $2,000–$4,000

- Loan establishment fees: $1,000–$2,000

- Stamp duty: 4%–6% of property value (varies by state)

For a $500,000 property purchase, you’re looking at roughly $35,000 to $50,000 in upfront costs beyond your deposit. These costs come from your SMSF’s available funds, so ensure sufficient liquidity exists before committing to the purchase.

Ongoing expenses include loan interest, property management fees (typically 7%–9% of rental income), council rates, insurance, repairs and maintenance, and annual SMSF administration and audit fees. Your fund must maintain sufficient cash flow to cover these expenses, even during vacancy periods. This is where serviceability assessment becomes critical—your rental income needs to comfortably exceed these ongoing costs, with buffer capacity for interest rate increases and unexpected expenses.

Aries Financial’s lending criteria require conservative serviceability assessments precisely because we understand these ongoing obligations. Our borrowing capacity calculations factor in stressed interest rate scenarios, ensuring your SMSF can service the loan even if rates increase by 2%–3%. This conservative approach protects your retirement savings from financial stress and potential forced sales.

Compliance Considerations and Risk Management

The LRBA structure offers powerful benefits, but it also creates compliance obligations that must be managed meticulously. The most common risks include:

The In-House Asset Rule: Your SMSF cannot have more than 5% of its total assets invested in in-house assets (loans to or investments in related parties). While your property acquisition itself doesn’t typically trigger this rule, funding arrangements need careful structuring to avoid inadvertent breaches.

The Sole Purpose Test: Everything your SMSF does must be for the sole purpose of providing retirement benefits to members. Allowing a member to use the property, even temporarily, violates this fundamental rule. We’ve seen cases where a member stored personal belongings in an SMSF-owned warehouse during a house move, triggering ATO scrutiny and penalties.

Prohibited Acquisition and Disposal Rules: You can’t buy from or sell to related parties (with limited residential property exceptions that are tightly constrained). Even well-intentioned transactions with family members can create serious compliance breaches.

Financial Planning Risk: Property investment concentrates risk. If your SMSF holds most of its assets in one or two properties, you lack diversification. Market downturns, extended vacancies, or property-specific issues can significantly impact your retirement savings.

At Aries Financial, we see our role extending beyond loan provision. We partner with accountants, advisors, and legal professionals to ensure clients understand these compliance requirements and maintain proper governance throughout their SMSF property investment journey. Our commitment to integrity means sometimes having difficult conversations—advising clients when a proposed structure creates unnecessary risk or when their fund isn’t suited for property investment.

Your Pathway to Strategic Wealth Building

Borrowing to buy property in your SMSF represents one of the most sophisticated wealth-building strategies available to Australian investors. When structured correctly and managed diligently, it allows you to leverage your superannuation savings, accelerate retirement wealth accumulation, and maintain control over your financial destiny.

The seven-phase timeline we’ve outlined—from strategic planning through to post-settlement administration—provides a realistic roadmap for what’s involved. Yes, it’s more complex than buying a residential home with a traditional mortgage. Yes, it requires professional guidance and careful compliance management. But for many investors, the strategic advantages far outweigh these additional considerations.

Aries Financial’s vision is simple: Empowering Australians to maximize their retirement potential through specialized SMSF lending solutions. With competitive rates starting from 5.99% PI, streamlined approvals within 1-3 business days, and deep expertise in SMSF compliance requirements, we’ve simplified a complex process without compromising on quality or compliance standards.

Whether you’re a seasoned SMSF trustee exploring your first property investment or an experienced property investor considering the SMSF structure for tax optimization, the key is partnering with professionals who understand both the opportunities and the obligations. Your retirement savings deserve nothing less than expert guidance, transparent communication, and unwavering commitment to compliance.

Ready to explore whether SMSF property investment makes sense for your retirement strategy? Connect with Aries Financial to discuss your specific circumstances and discover how strategic borrowing could accelerate your wealth-building journey. Because at the end of the day, your retirement should be about enjoying the fruits of your labor—not stressing about whether you’ve structured your investments correctly.