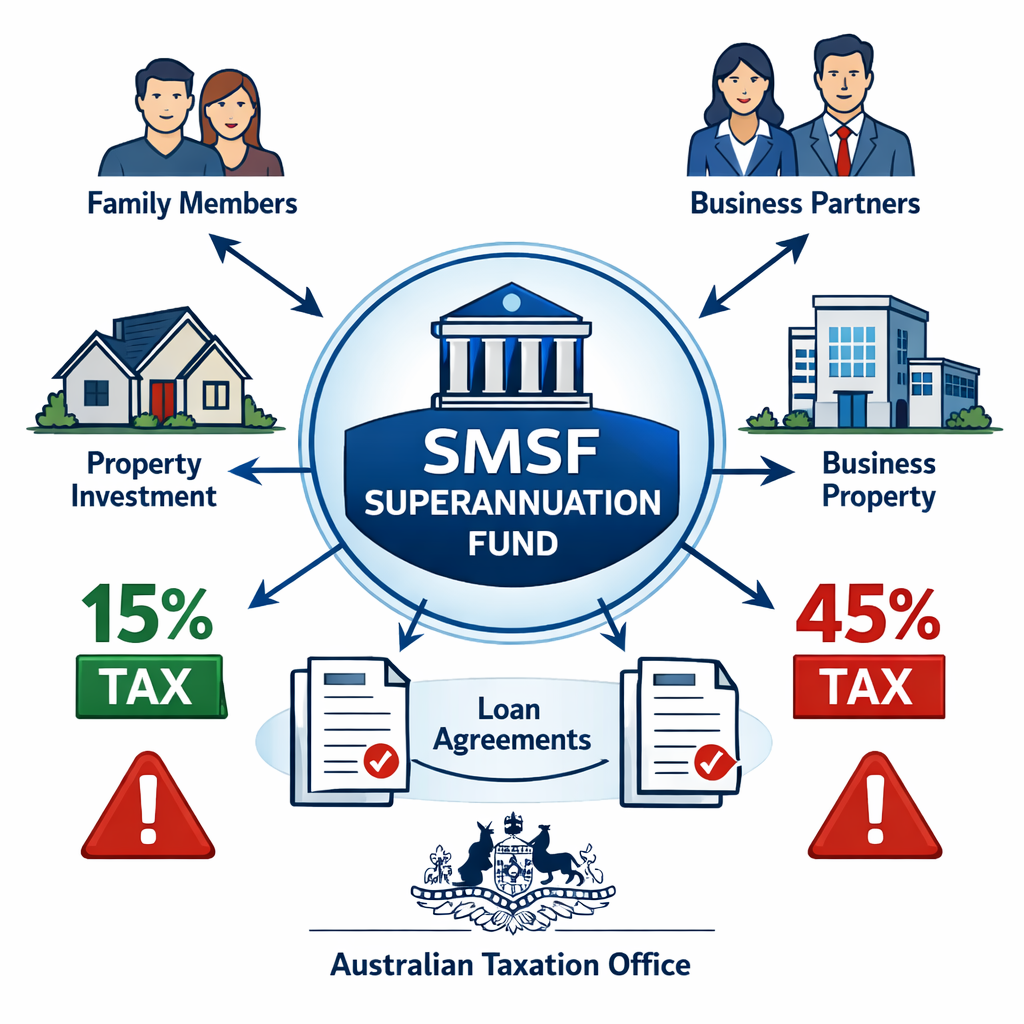

Family loans for SMSF property can trigger devastating tax penalties if arm’s-length terms aren’t met. The ATO’s non-compliance consequences include 45% tax rates instead of 15%—learn how to protect your retirement savings from related party borrowing risks. #limited recourse borrowing smsf related party