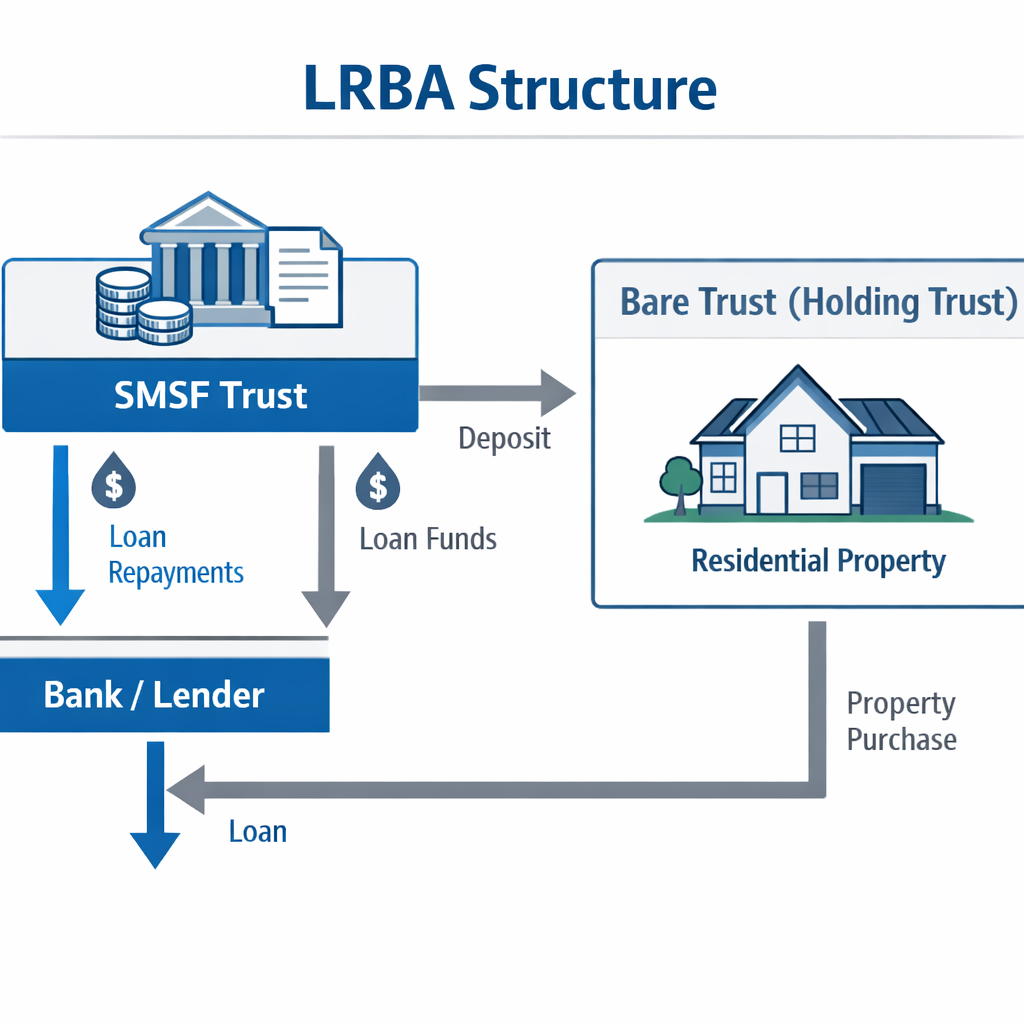

SMSF trustees exploring property investment need to understand the limited recourse borrowing arrangement definition—a specialized structure allowing super funds to borrow while protecting retirement assets. Learn the compliance requirements, risks, and opportunities before you leverage your super.

#limited recourse borrowing arrangement definition