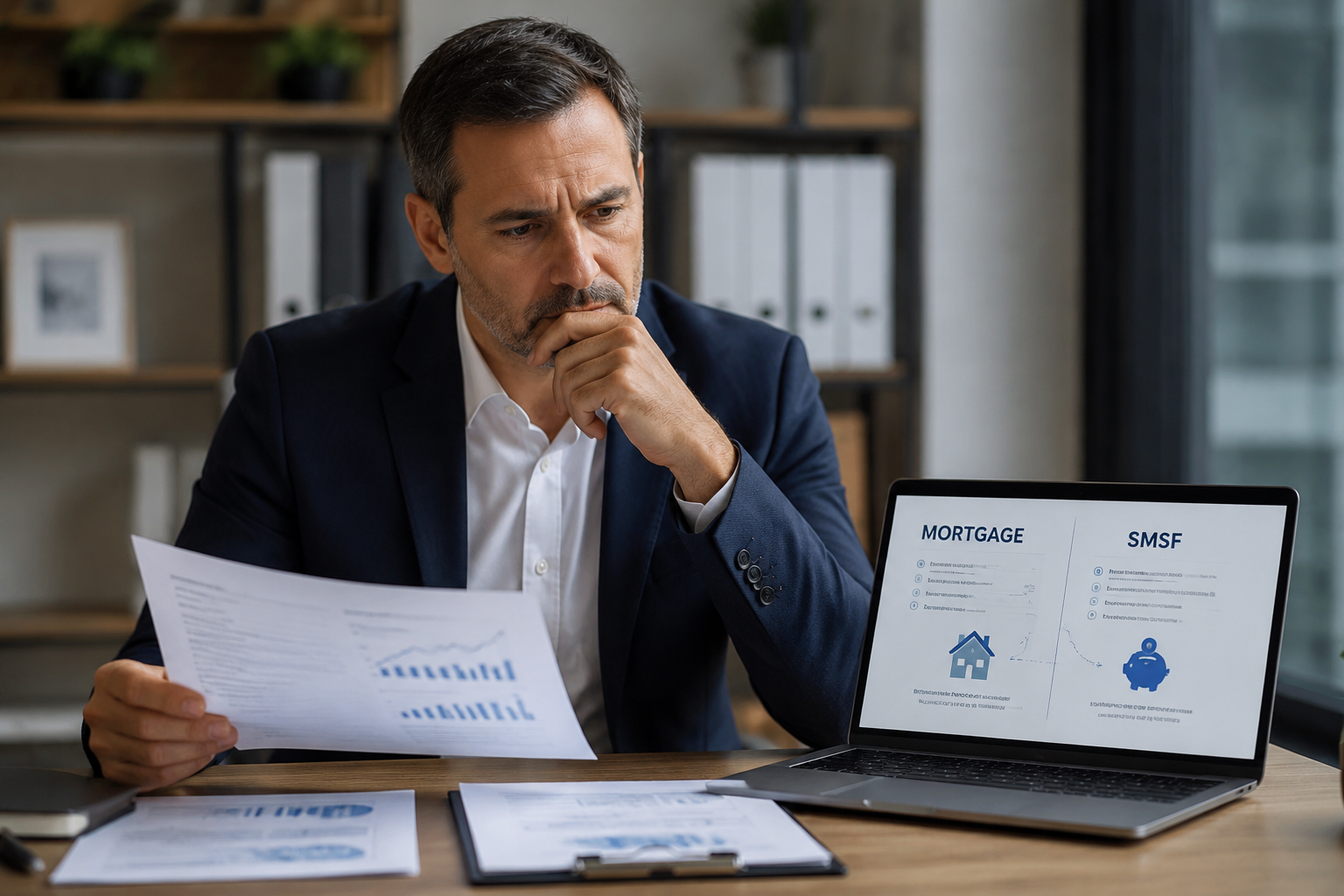

Your existing mortgage doesn’t legally cap SMSF borrowing, but it quietly drains the cash flow needed for contributions that fuel loan servicing. The hidden trap? Cross-securitization and informal arrangements trigger devastating NALI penalties at 45%. Smart trustees model total debt exposure and maintain absolute separation between personal and super finances.

#smsf borrowing capacity existing mortgage